How is embedded insurance different from any other revenue layer property businesses have added?

It is not different. It is the same adjacent-monetisation play platforms have run before with payments, lending, and premium listings. Protection is the next unclaimed layer on top of the core product, not a new business model, and it is measured with the same commercial vocabulary.

Product leaders already think in ARPU, customer lifetime value, and attach rate. Embedded protection extends those metrics rather than introducing a foreign one. The Chief Product Officer who added a payments layer or a lending partner has already made this decision once. The structural logic is identical: own a high-intent moment, monetise it inside the journey, measure it on the metrics that already sit on the scorecard.

Does adding protection mean becoming an insurer?

No. Our platform Kanopi owns the customer moment, the insurer owns the risk, and an orchestration layer connects them. The compliance and underwriting burden sits with the insurer, not the platform, and protection operates alongside existing systems without a core rebuild.

It is important to clarify that this model does not constitute broking. Because the platform facilitates the connection rather than acting as a broker itself, there is no requirement to obtain additional licenses or undergo separate compliance processes.

This is the distinction that matters to a product organisation weighing the opportunity against the operational cost. Kanopi is a full insurance platform with AI-native tooling that lets protection be introduced, tested, and deployed alongside what a platform already runs. There is no new licence to hold, no new compliance team to staff, and no replacement of the systems the platform depends on. The revenue layer is added; the operating model is not disrupted.

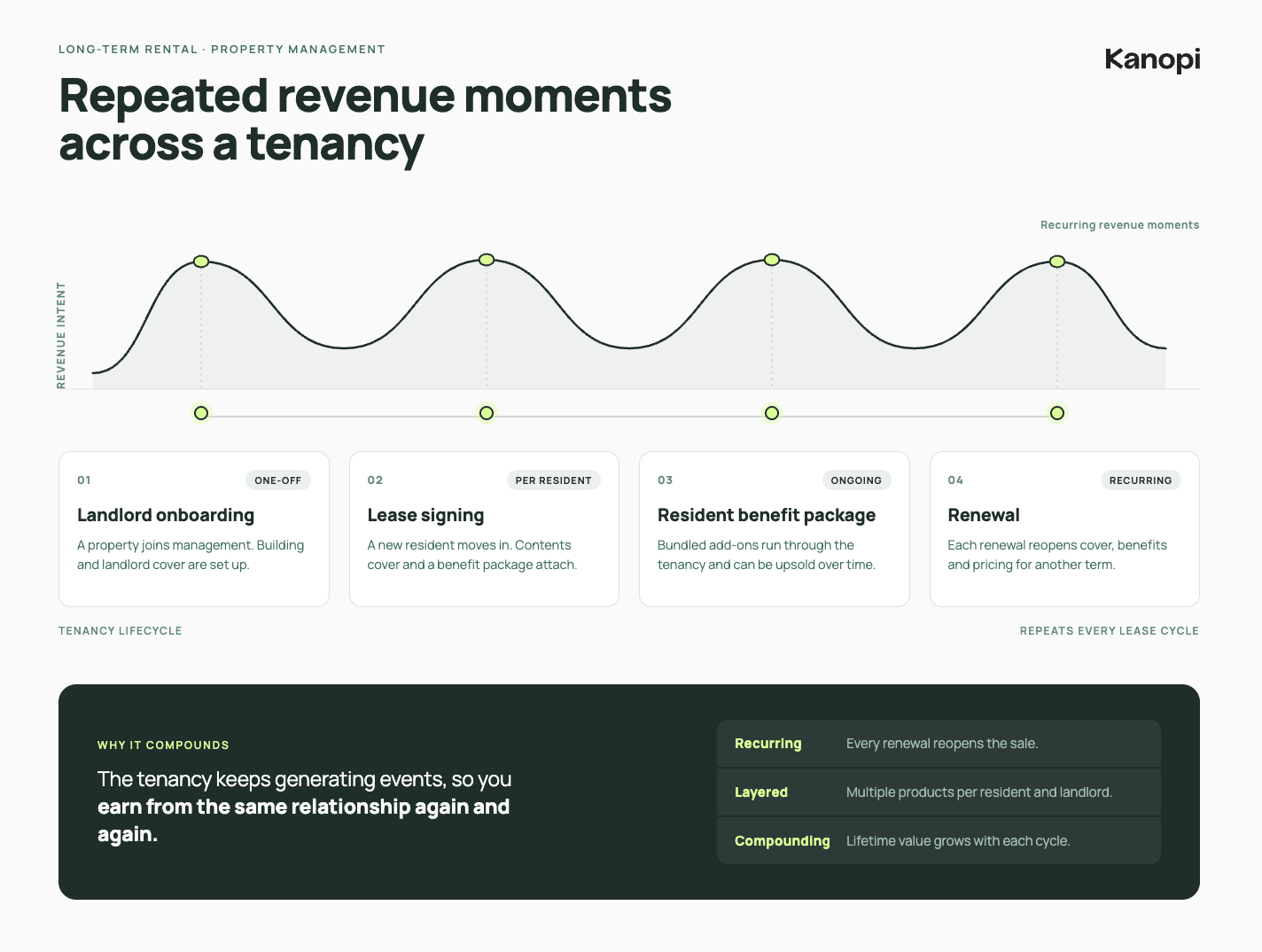

Which property platforms are best positioned to capture this?

Digital platforms, digitally enabled businesses, growth focused companies that already own a mandatory or recurring insurance moment are best positioned. That includes real estate listing portals with a settlement window and rental or property management platforms with lease and renewal cycles.

How proptech platforms lift ARPU with embedded insurance

Maria De Orueta, former GM at PiP / SGUA, on how platforms that proactively embed insurance into their property journeys see a significant uplift in ARPU.

The prerequisite is not scale or an insurance background. It is ownership of the moment where cover becomes necessary. A portal such as REA Group or Domain owns the settlement window. A rental agency owns the lease. Both already generate the demand.

The capability gap is not demand creation, which is the hard part and is already solved. It is capture.