A security deposit looks deceptively free to administer.

For a property management business, the deposit sits at the centre of a web of manual work: collecting it, holding it, verifying certificates of insurance against it, arbitrating disputes over it, and refunding it.

None of that shows up as a line item, so it reads as the cost of doing business. But, it doesn’t have to be. It’s a process that was never built to scale, and it is one of the largest hidden operational drags in residential property management today.

Most property managers treat deposit collection, dispute handling, refunds, and certificate-of-insurance chasing as four separate annoyances. They are not four problems. They are one system, and it grows heavier with every door added to the portfolio.

What does the security deposit actually cost to administer?

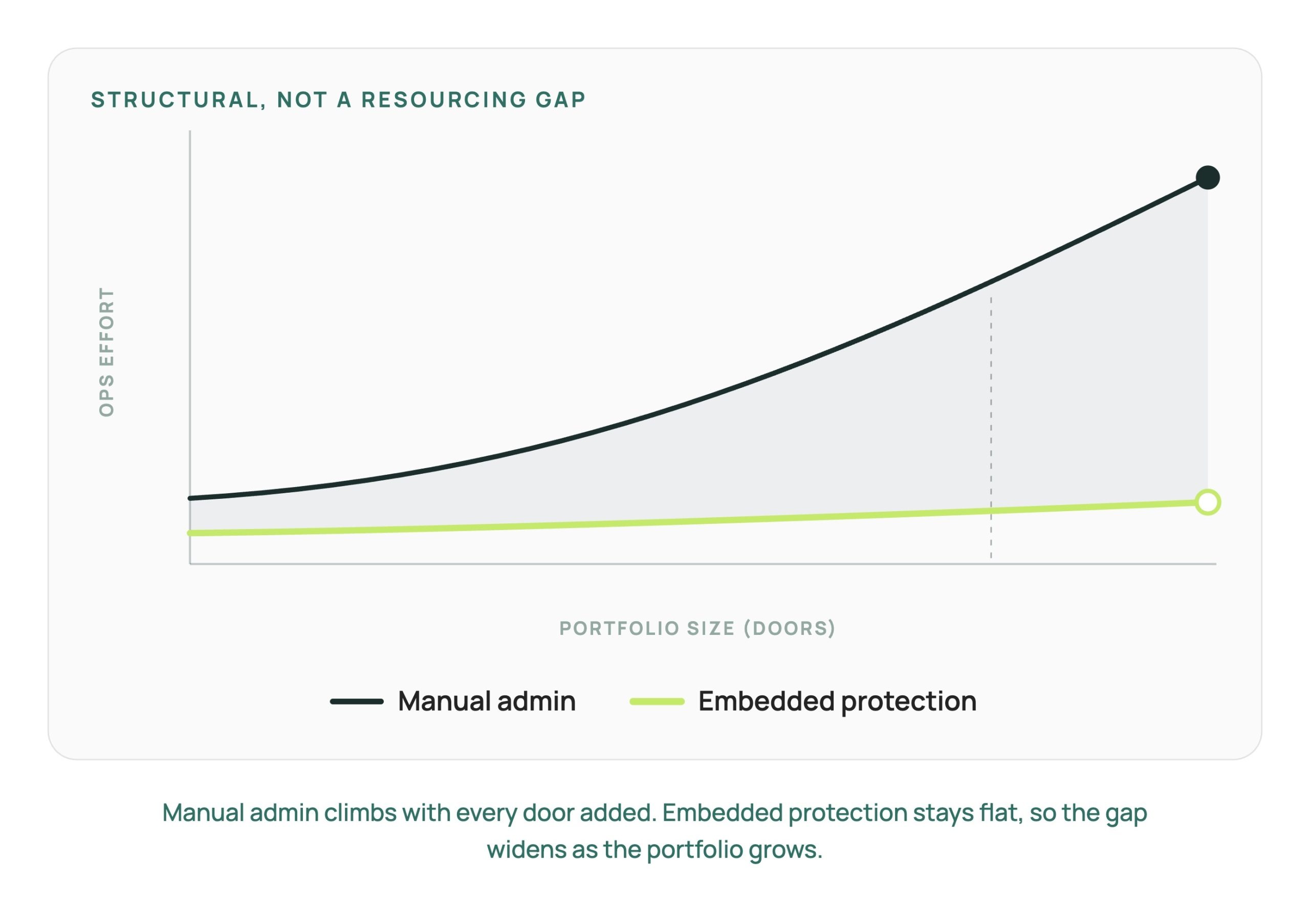

The deposit costs staff time at every stage of its lifecycle, and that time scales linearly with the portfolio while the team does not. Collection, holding, verification, dispute resolution, and refund each consume hours that never appear on a balance sheet.

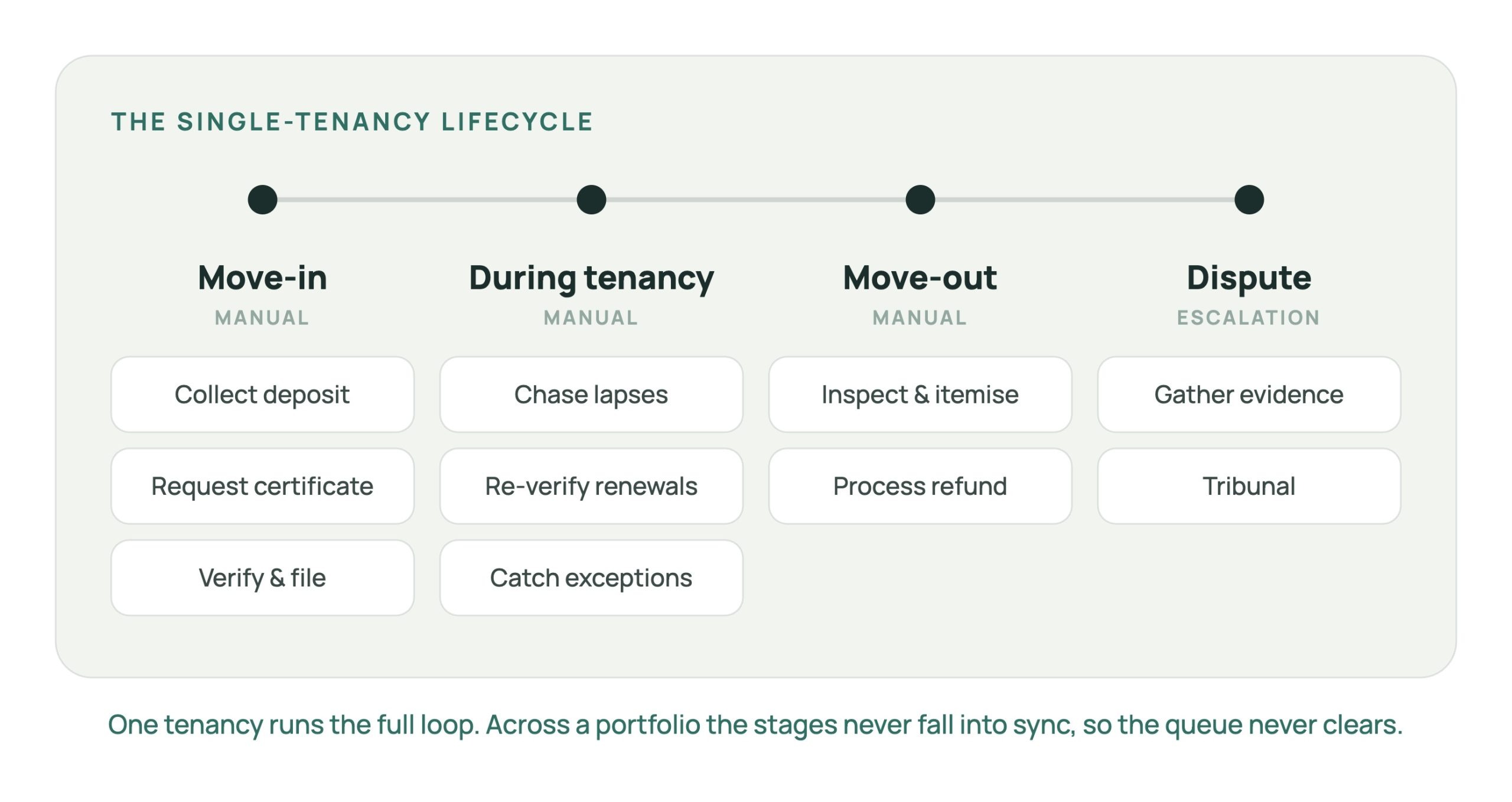

Walk the lifecycle of a single tenancy. At move-in, the team collects the deposit, records it against a trust or holding account, and requests proof of contents or liability cover. It then verifies that certificate is valid and current, and files it.

Through the tenancy, it chases certificates that lapse and re-verifies renewals. At move-out, it inspects, itemises deductions, and processes the refund. If the tenant disputes a deduction, the matter escalates into correspondence, evidence gathering, and sometimes a tribunal.

Why does certificate-of-insurance chasing never get easier?

Certificate-of-insurance chasing never gets easier because it is a manual verification loop with no natural end state.

Every new tenancy adds one. Every renewal resets one. Every lapse creates an exception that a human has to catch and correct.

The work is relentless, not difficult. A property manager collects a certificate, checks the coverage type and expiry, confirms the named parties are correct, and files it. Then a policy lapses mid-tenancy and the loop restarts, except now it is an exception that has to be noticed before it becomes a liability. Multiply that across a portfolio and the verification queue never empties. Adding staff moves the queue; it does not remove it.

This is the tell that the problem is structural rather than a resourcing gap. A resourcing problem gets solved by hiring. A structural problem gets worse as you grow, because the work is generated by volume, not by effort.

What is the hidden cost of chasing certificates, beyond staff hours?

The hidden cost is lost continuity with the customer and exposure the business carries without pricing it. Manual verification means gaps go unnoticed. Deposit disputes sour the end of a tenancy. And every time a tenant is sent off-platform to arrange their own cover, the business loses sight of them at the moment it should be reinforcing the relationship.

Consider three costs that never reach a spreadsheet.

- Coverage gaps. A lapsed certificate that no one catches is uninsured exposure sitting inside the portfolio until a claim reveals it.

- Relationship erosion. A deposit dispute is often the last interaction of a tenancy. It is a poor note to end on, and it colours renewal and referral behaviour.

- Broken continuity. When a tenant leaves to source cover elsewhere, the business hands the relationship to a third party at a decision point it created.

Each of these is a cost the business absorbs quietly. None of them is captured in the headcount figure that ops leaders are usually asked to defend.

How does embedded protection remove the process rather than the workload?

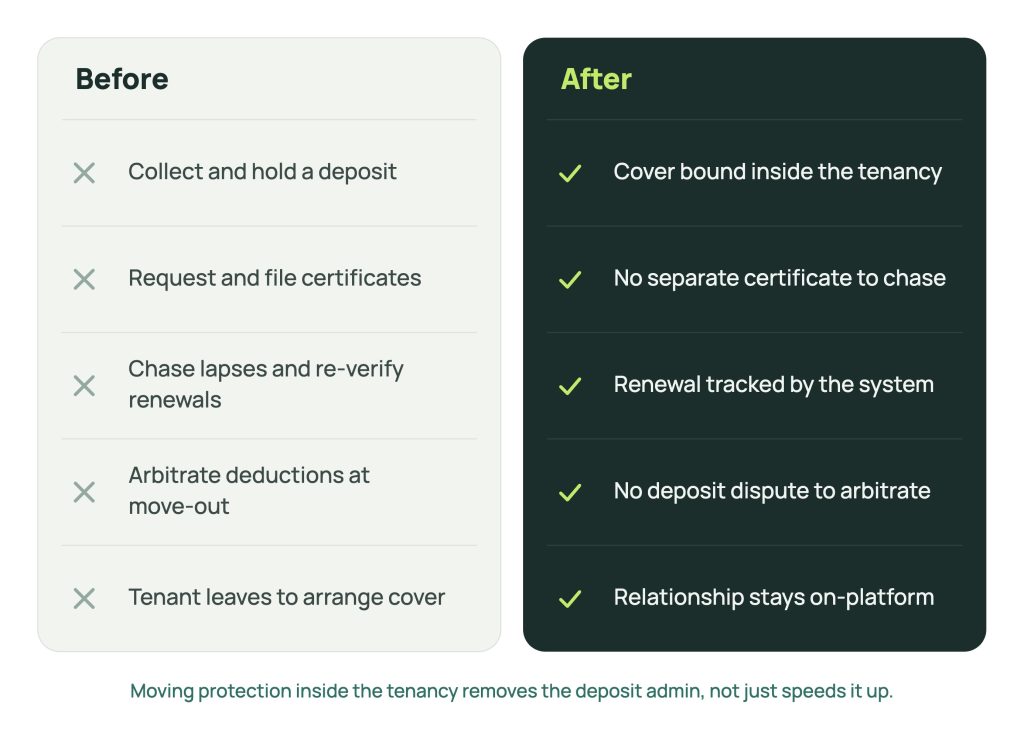

Embedded protection removes the process by replacing the manual artefact entirely. When cover is arranged inside the tenancy journey, there is no separate certificate to collect, verify, chase, or reconcile against a deposit. The verification loop does not get faster. It stops existing.

This is the distinction that matters. Automation of the existing process still leaves the process in place: a faster chase is still a chase. Embedded protection changes the artefact. Cover is bound at the point of the tenancy, tracked by the system that arranged it, and renewed without a manual re-verification step.

The security deposit’s role as an informal insurance mechanism, and all the administration that role generates, can be traded for coverage that lives inside the business.

Does removing the deposit process mean becoming an insurer?

No. The platform owns the tenancy moment, the insurer owns the risk, and an orchestration layer connects them. The compliance and underwriting burden sits with the insurer, not the property management business, and protection operates alongside the systems the business already runs.

It is important to clarify that this model does not constitute broking. Because the platform facilitates the connection rather than acting as a broker itself, there is no requirement to obtain additional licences or undergo separate compliance processes.

Kanopi is a full insurance platform with AI-native tooling that lets protection be introduced and deployed alongside existing property management systems. There is no new licence to hold and no core system to replace. The manual verification process is removed; the operating model is not disrupted. For an operations leader, this is the point: the workload disappears without a migration project attached to it.

The admin was never the job

The security deposit and its surrounding administration were never the work a property management business set out to do. They were a workaround for a risk that could be covered more directly.

Deposit collection, dispute handling, refunds, and certificate chasing are not four separate costs to be trimmed. They are one systemic drag that can be designed out by moving protection inside the tenancy journey.

For the business, that means fewer manual queues, less unpriced exposure, and a customer relationship that stays on-platform through the moments that used to send it away.